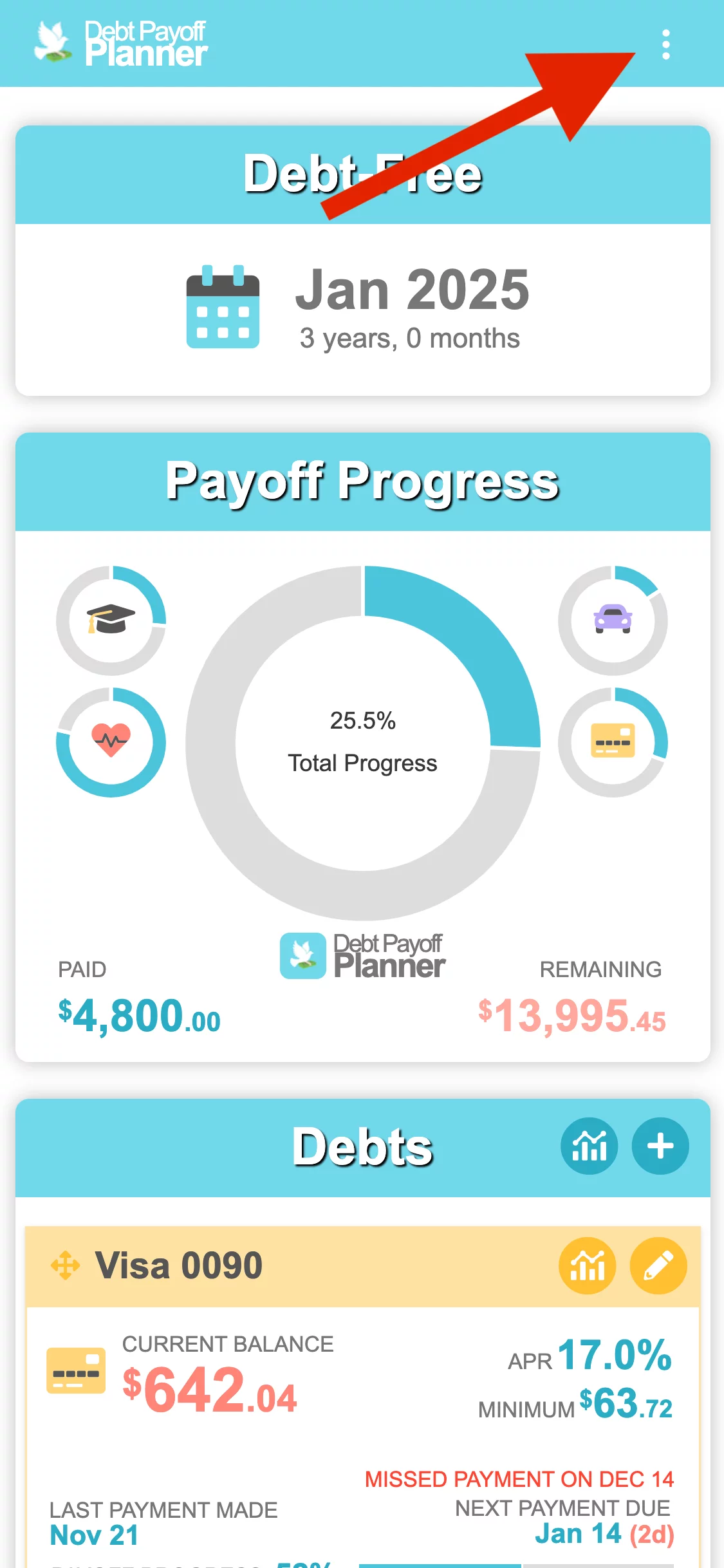

As you progress with your payoff, you will use the plan provided by the app as a guide for how to make your payments. Once you make a payment to a creditor, you should record this payment in the app so that your progress indicator reflects the payment you made and the payment due date indicator reflects the next payment date.

You record your payment in the app by doing the following:

- Tap on the debt that the payment was made to in order to show the Edit Debt dialog

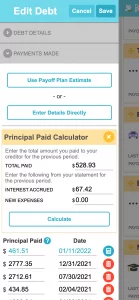

- Tap on the calculator icon to show the details of how the principal paid is calculated

- Tap on the “Use payoff plan estimate” button to fill the calculator with the details from the plan

It’s important to note that only the principal portion of you payment is recorded. Any component of your payment that goes to interest should not be included here. This is done because your balance and progress is determined by the amount of principal paid, not the total payment you paid to your creditor.

If the values in the estimate do not match the statement from your creditor, make changes as needed and then top “Calculate”. Once you are happy that the principal paid reflects the right value, tap “Save” to record your payment.

A payment to your creditor has two components. Part of your payment goes toward paying the interest due, and the remainder of your payment goes toward you principal amount owed. While the Payoff Plan shows the estimated total payment (both interest and principal) to make to your creditor, the payment tracking feature of the app is for recording only the principal component.

You can record the estimated principal amount that the app has determined by tapping “Use Payoff Plan Estimate” and tapping “Enter Details Directly”. This will show a handy principal paid calculator with the estimates pre-populated from the plan. You should review the accuracy of this against your actual statement and adjust the estimated values as necessary. Once the values are correct, tap “Calculate” to fill in the principal payment, and the click “Save” to save the payment and see your progress made.

No, the app will NOT connect to any of your accounts and therefore is not aware of the payments you make until you enter that information into the app. To record the payment you have made, do the following:

- Tap on a debt to open the “Edit Debt” dialog

- Tap on “Payments Made” to open the payment tracker

- Enter the amount of the principal paid

Note that the “Principal Paid” will be different than the total payment amount due to interest. See the question about determining “Principal Paid” if you need help with this.

If you have new expenses in an account, such as a credit card, which increases the amount of debt for that account, you can inform the app of this change by using the payment tracker. Typically, you would enter a positive number in the payment track to record a payment that reduces the principal owed (i.e. the debt balance for the account). For new expenses, enter a negative amount, which will increase the debt balance for the account and update your plan based on the new balance.

The balance reflected in the app should match your statement in many cases, however, it may differ from your account statement from your creditor for various reasons. For example, interest calculations may vary slightly, you may have added expenses that the app is not aware of, or you may be coming back to the app after having not used it for a while. If you need to adjust your current balance to match your statement you have two options:

- You can directly change the original balance you set for the account in the debt details settings.

- You can record a positive or negative “payment” for that account, which will change your balance. The amount of this payment should be calculated as follows: payment_amount = current_balance_in_app – current_balance_from_statement

The best approach to use is #2, record a payment to reconcile the balances. Doing this ensures that your progress is reported correctly.

No, the app does not change the monthly payment budget when a debt has been paid off.

Your planned monthly payment is the total of both your minimum required payment and an extra amount you want to pay toward your balances. When you completely payoff a debt, you no longer need to make payments to that account and your payoff plan will show this. Even though you are no longer required to make minimum payments on that account, the app will continue to include the minimum payment that was set for the paid off account as part of your planned monthly payment budget and the plan will allocate that budget to another account. This roll-over of you payment budget is an important part of the debt snowball and debt avalanche payment methods.

If you prefer to reduce your planned monthly payment each time you payoff a debt, you just need to change the minimum payment for the paid-off account to $0. This will reduce your planned monthly payment, but keep in mind that this will change your plan and make your payoff take longer.

If you are temporarily not making payments on a loan, you should do the following in order to ensure the app is taking this into consideration when calculating your due dates and proposed payment plan. When you loan is on pause, continue to record payments as you normally would, except you should enter $0 as the payment amount and enter the next due date as the payment date. Entering this $0 payment will force the app to consider the current month as paid and will update the due date to the next month. If you loan is not accruing interest while it is on pause, you should update you loan details in the app to reflect a 0% APR until such time that your loan begins accruing interest again.

When you add a snowflake payment to your strategy, your plan will contain a one-time payment in the amount you specified on the date you entered. Once you make your snowflake payment, you should record this one-time payment in the “Payments Made” section of the edit debt dialog. After recording the payment, you should delete the snowflake payment from your strategy section.

There is no option within the app to change your email address, which is also used for your login username. However, our support team will be happy to make the change for you. To request the change, please do the following:

- Send an email to support@debtpayoffplanner.com from the email address you are currently using with your request to change your email address

- Send a second email to support@stebt.com from the email address you want to change to with your request to change your email address

- In each email the body of the email should contain the same request text

We use this procedure to ensure that changes we make on behalf of users are valid requests to ensure your data stays secure.

If you no longer have access to the email address currently being used, we can validate your account through other means. Please email our support team at support@stebt.com and they will provide further instructions.

Yes, two people can each have the app installed on their respective device and access the same information as long as you have created an account (i.e. you cannot be using a guest account) and both people login with the same username and password.

Create Account Page:

Please note that if you purchased a pro membership directly through our website instead of Google Play, then you will NOT automatically be charged at the end of your term and these instructions do not apply to you.

If you have upgraded to a pro membership through Google Play and wish to cancel your subscription, you may do so through the Google Play app, or through play.google.com by following these instructions.

Cancel a subscription on the Google Play app

Note: Uninstalling the app will not cancel your subscription.

- On your Android phone or tablet, open the Google Play Store.

- Check to make sure you’re signed in to the correct Google Account.

- Tap Menu > Subscriptions.

- Select the subscription you want to cancel.

- Tap Cancel subscription.

- Follow the instructions provided.

Cancel a subscription online

Note: Uninstalling the app will not cancel your subscription.

- Go to play.google.com.

- Check to make sure you’re signed in to the correct Google Account.

- At the left, click My subscriptions.

- Select the subscription you want to cancel.

- Click Manage > Cancel Subscription.

- Within the confirmation pop-up, click Yes

For more information regarding subscriptions billed through Google Play, please visit their support center here.