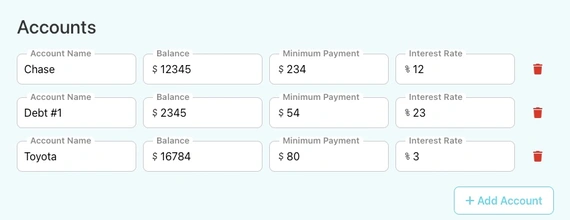

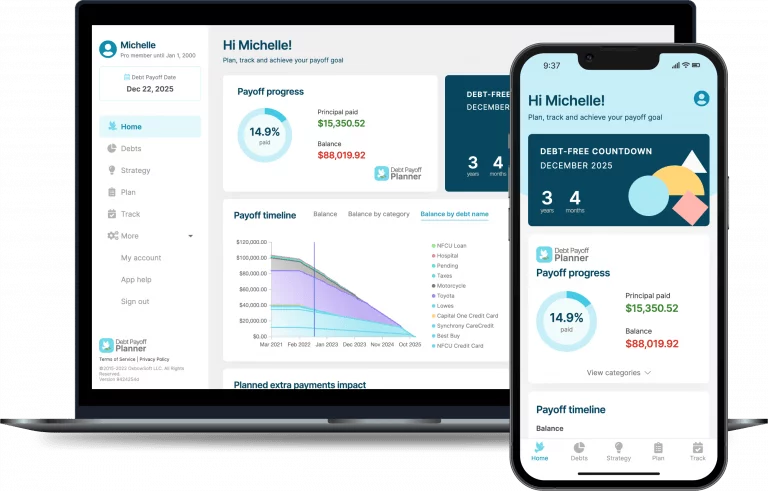

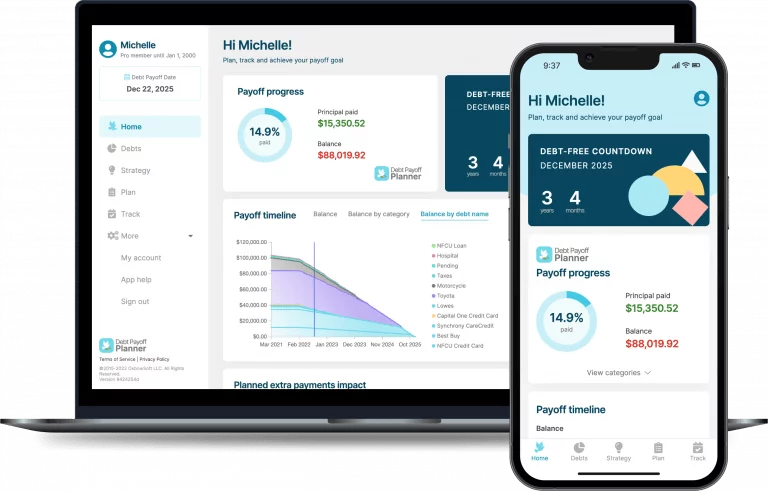

Accounts

$

$

%

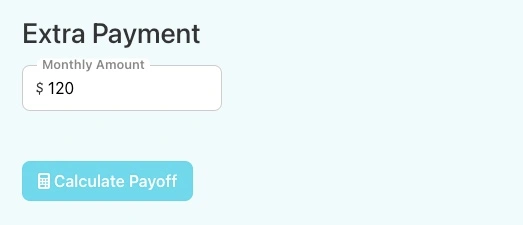

Extra Payment

$

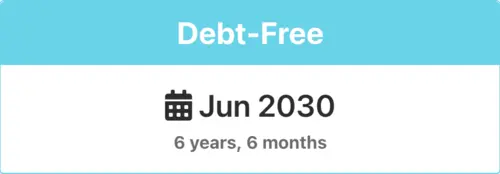

Debt-Free

Sep

2025

1 year, 6 months

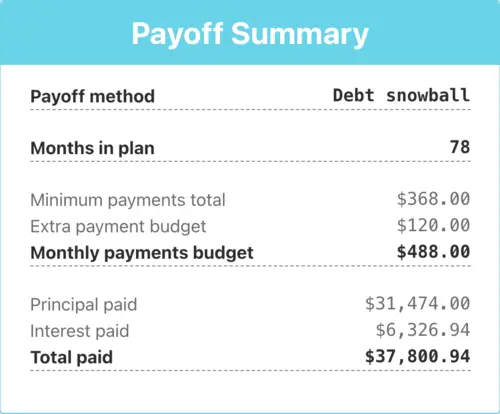

Payoff Summary

Payoff methodDebt snowball

Months in plan$123.45

Minimum payments total$123.45

Extra payment budget$123.45

Monthly payments budget$123.45

Principal paid$13,234.00

Interest paid$1,674.98

Total paid$13,234.00

Debt Payoff Planner App

Enjoying this debt snowball calculator?

Then you'll love the Debt Payoff Planner app

Debt Payoff Planner is the most comprehensive app for planning and tracking your debt payoff

and has helped over 1 million people achieve less stress, more motivation, and a faster payoff.

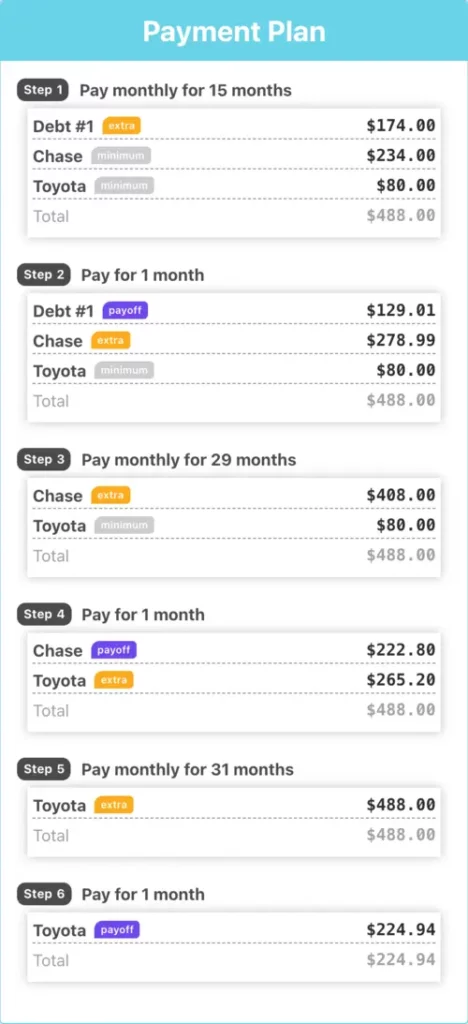

Payment Plan

Step

1

2 months

Step

1

Duration

2 months

Debt

Payment

Surgeryextra

$100.00

6

minimum

payments

$1341.28

JC Penny

$3.72

Visa 0090

$63.72

BofA 3342

$13.37

Student loan #1

$125.00

Toyota loan

$135.47

Debt #7

$1,000.00

Total

$1441.28