Debt Snowball Method

Debts cause financial, emotional, and even physical struggles, but paying it off seems impossible.

What if you could create a roadmap toward debt freedom with a simple method?

The debt snowball strategy is easy enough for anyone to use – even consumers living paycheck-to-paycheck.

It’s a motivational program that encourages ‘quick wins’, which may motivate you to keep going. If your primary concern is the emotional toll that the debt-trap has us in, then check out the snowball method below.

What is the Debt Snowball Method?

Put simply, the debt snowball method helps you reduce your debts. But it’s more than that – it’s a way to change how you look at money.

Up until now, did you feel like debt controlled your money? You only had as much money left as your debt would allow, right?

The debt snowball method turns that around. You focus on one debt at a time, earning those ‘quick wins.’ Suddenly, managing your money seems not only easier but completely possible.

Snowballing debt is the fastest way to reduce and/or eliminate it. With this new ‘outlook’ on money management, you can avoid getting into debt again, and instead, realize saving for what you want is more than possible.

How Does Snowballing Debt Work?

Snowballing debt is as easy as creating snowballs when you were a kid using these steps:

- Put your debts in order from smallest balance to largest

- Write down the minimum payment for each debt

- Work each minimum payment into your monthly budget

- Determine how much ‘extra’ money you have each month and pay it toward the first debt in line (in addition to the minimum payment)

- Keep doing this until you pay the first debt in full

Congratulations! You’ve paid off your first debt! Celebrate your ‘small win’ and keep the momentum going. Seeing how easy it is to tackle that first debt should ‘snowball’ into the next debt.

Take the exact amount you paid to the first debt (the now paid off debt) and add it to the minimum payment you’re paying for the 2nd debt. Keep doing this for each debt until you’ve created such a large snowball that you’re completely out of debt.

What Debts Should you Include?

Your debt snowball plan may include any non-mortgage debt. All consumer debt is fair game, including:

- Credit cards

- Personal loans

- Medical bills

- Car payments

- Student loans

Example of Snowballing Debt

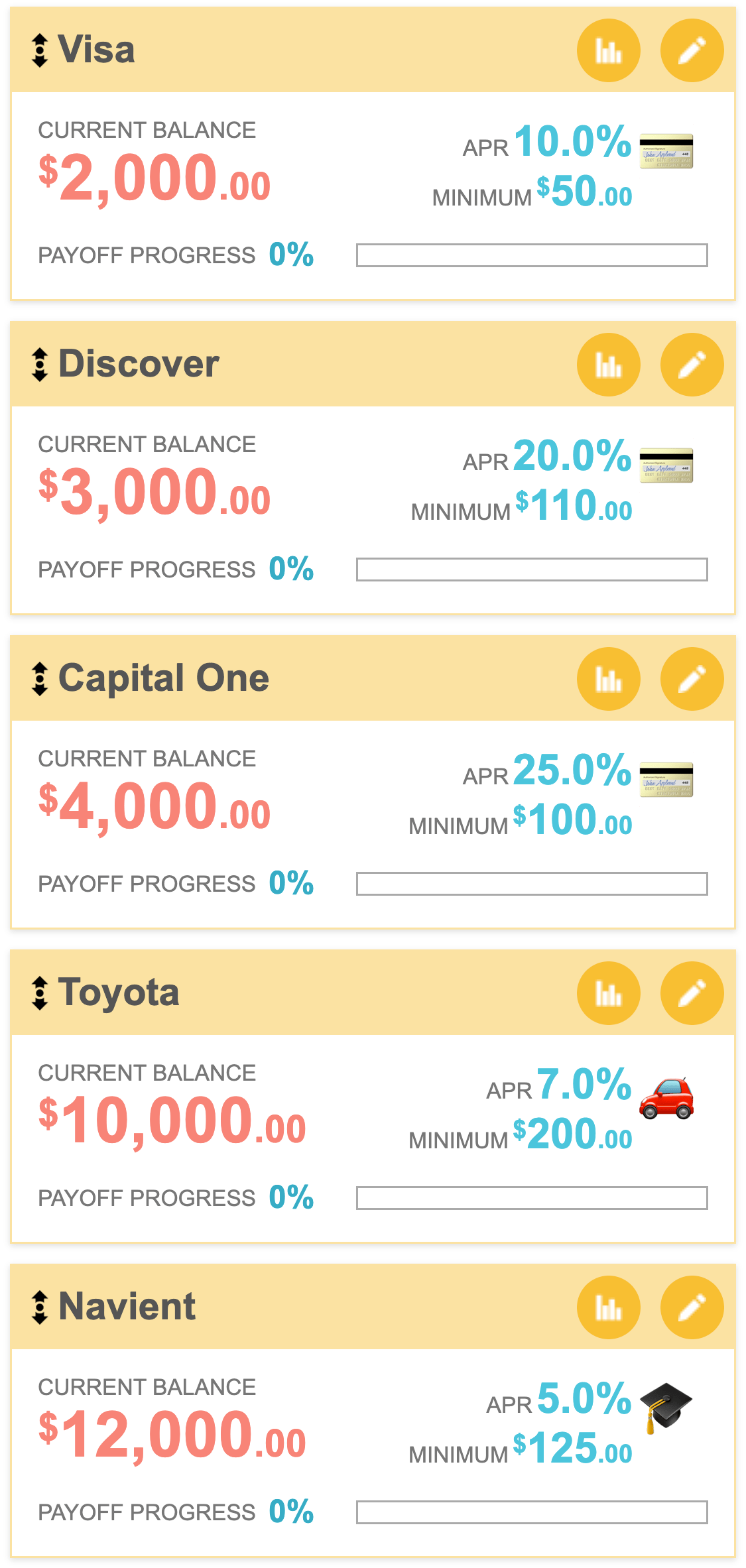

John has the following debts that he’d love to pay off:

- $2,000 credit card – $50 minimum payment

- $3,000 credit card – $110 minimum payment

- $4,000 credit card – $100 minimum payment

- $10,000 car payment – $200 payment

- $12,000 student loan – $125 payment

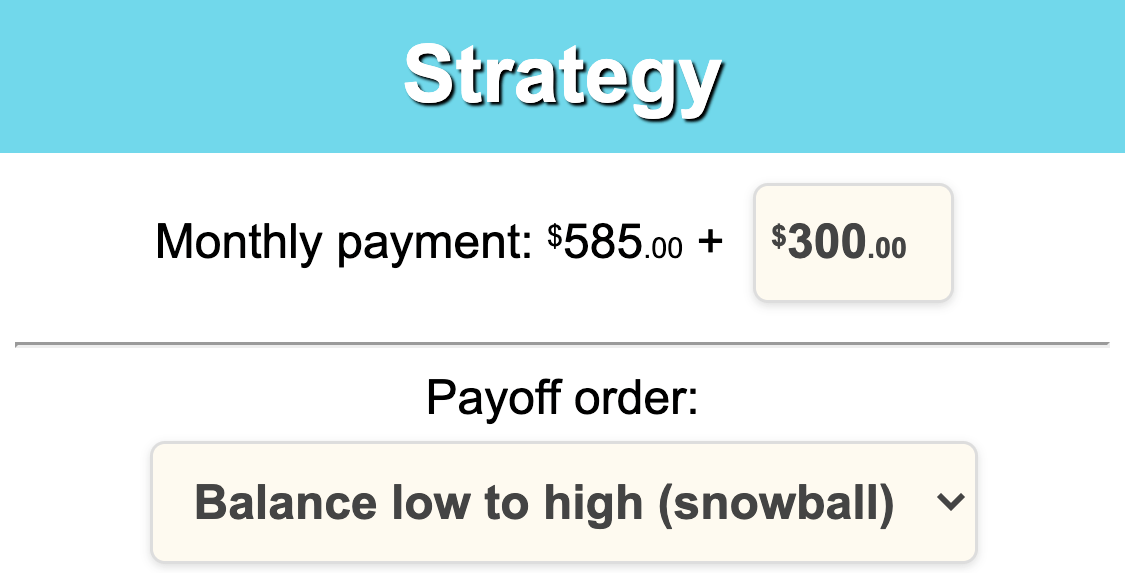

John budgets the minimum payments for each debt monthly. He cut his expenses down by cutting the cord, finding cheaper insurance, and eliminating bank fees. His ‘found money’ is $300 extra a month on top of the minimum required payments.

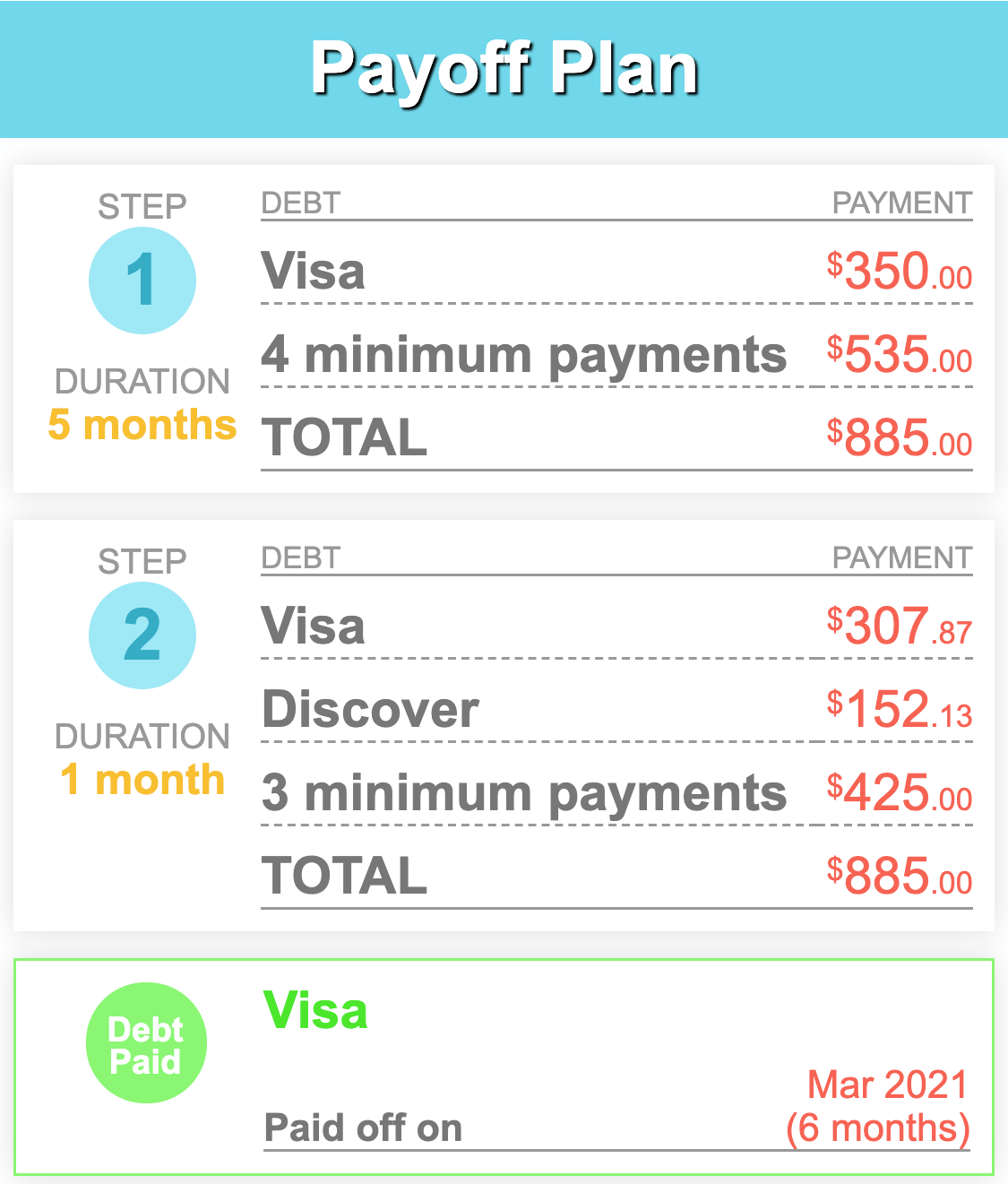

John pays $350 a month to the first credit card ($2,000 credit card), paying it off in about 6 months! Great job!

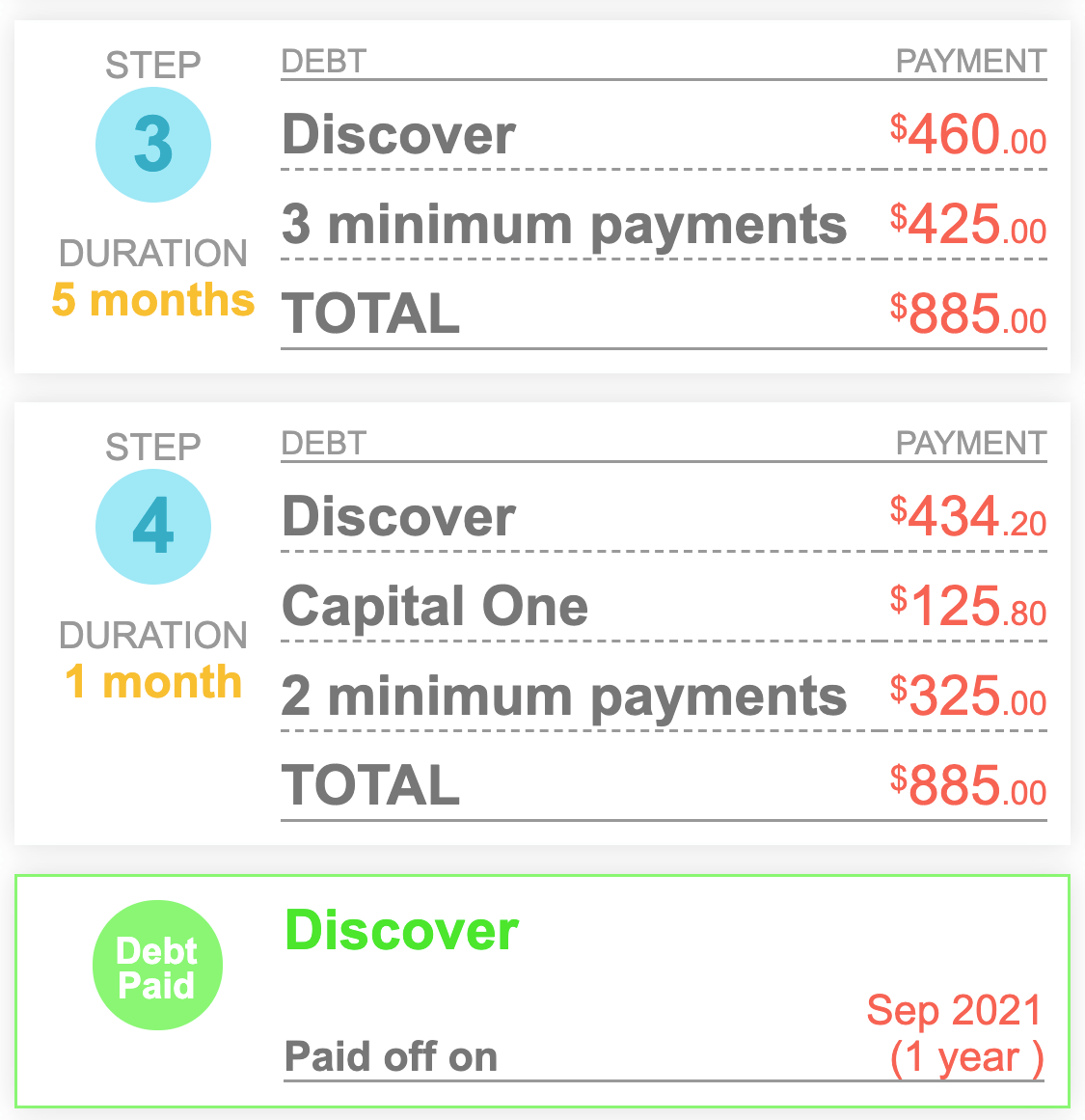

Now he keeps the snowball going by paying $460 a month to the $3,000 credit card ($350 + $110). It takes him just about 6 additional months to pay that debt off in full.

In just about a year, John’s already paid off two credit cards and paying $560 to the third and last credit card. In just about an additional 7 – 8 months, John is completely out of high-interest credit card debt and now sends $760 a month to his car payment and then finally $885 a month to his student loans.

In a matter of a few years, with great dedication, John got himself out of consumer debt and can hyper-focus on saving for retirement and/or paying off his mortgage.

Benefits of the Snowball Method

- It’s motivational – Paying off even a small debt feels amazing. When you see the plan working, you’re more likely to keep going. Paying just the minimum payments makes you feel like you’re on a hamster wheel going nowhere, but the debt snowball method ends that.

- Easy to implement – Anyone can start the debt snowball themselves. You don’t have to pay financial advisors or generate extra income. Just input your debts into The Debt Payoff Planner and start following the payoff plan.

- Keeps you organized – Debt is overwhelming. Seeing all the bills and minimum payments makes it hard to figure out which bill you should pay first. The snowball method creates a method out of the madness, helping you feel in more control.

- Easy to budget – Budgeting is hard enough, but if you add an excessive amount of debts and random payments, it gets harder. The debt snowball sets the parameters right from the start. Stick with the same payment (adding it to the minimum payments) each month and you have a predictable budget. Of course, if you have more money to contribute, you may always add to it.

Is the Debt Snowball Method the Best?

The best debt payoff program is the one you’ll use consistently. The debt avalanche method often gets higher accolades because you pay off high-interest debt first, but it’s not right for everyone.

Think about what motivates you the most. If you prefer ‘quick wins’ and motivation, the snowballing debt creates the fastest results. If paying high-interest rates causes you to lose sleep at night, consider the debt avalanche method instead.

No matter the method you choose, stay consistent. It may get frustrating to dedicate so much money to your debts, but when you pay them all off in a matter of a few years rather than a few decades, you’ll reap the rewards much faster.

Without debts, you can save a larger emergency fund, for a vacation, house, college, or retirement. Debts only eat away at your goal potential, but the debt snowball method provides a way out.

Related

Debt Avalanche Method

The debt avalanche or ‘debt stacking’ method pays off your debts with the highest interest rates first. Unlike the debt snowball, which focuses on balances, the avalanche method focuses on interest rates.

Start a Hustle for Extra Income

Extra income can help you speed up your debt payoff. This article highlights six side hustles to earn extra income without a lot of time.

6 Ways to Up Your Financial Game Now That You’ve Got a Debt Payoff Plan

You've crushed your debt-free planning using Debt Payoff Planner. These six tips from debt payoff champ Kelly Blodgett are great next steps to consider.