The Bank Of Mom And The Bank Of Dad

As I have been working with the great people at Debt PayoffPlanner, we have been having fun looking through data. One thing they pointed out to me was some interesting statistics relating to family loans. Often these loans are from a parent, which isn’t surprising, but something that did surprise me is some of them have an interest rate. In other words, the parents are charging their kids for their loans, which I found really surprising. Let’s dig into the data a bit more, and find out who lends their kids more often, Mom or Dad? And who charges more?

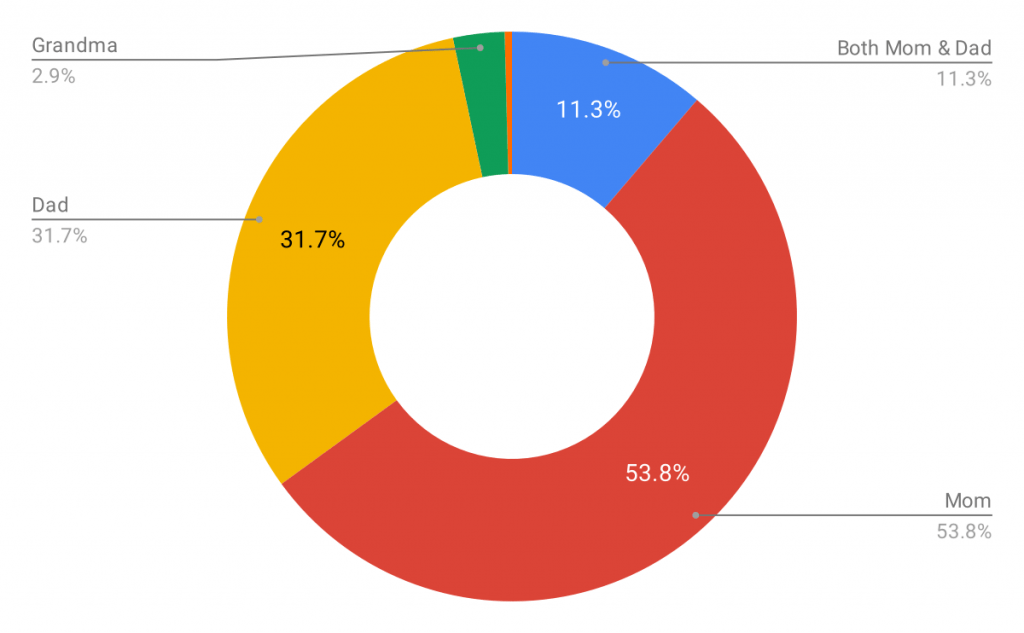

When we tallied up the data for 10,000 loans we found that the percentage of loans that were from “Mom & Dad,” “Mom,” “Dad,” “Grandma,” or “Grandpa,” was about 2.4%. That number may skew a bit low because it would make sense for folks to not add family loans into their debt payoff calculator especially if they aren’t being charged interest. We also might have missed some that were labeled differently, so we don’t want to take this data as gospel. But let’s take a closer look at the data we do have. Who loaned the most often?

Mom holds more than half of the loans, more than all the other family loans combined!

We then looked a little closer, and we noticed something strange. Most of the loans are at 0%, but we did notice a scattering of loans with an interest rate! But when you look at them you’ll find that only one of the interest-bearing loans is from “Mom & Dad” (for <2%), one for Dad (for < 4%) and all the rest are from “Mom”! And not only that, Mom’s interest rates ranged all the way up to 20%! I have to say, I’m completely stunned by that news. I guess Mom really knows how to put the screws to their kids (I’m kidding! Just kidding!). We have no way of knowing why some of these parents are charging such a high interest rate, but it does put a bit of a spin on what I thought I knew about family loans.

Paying off Family Loans

This is all very interesting, but the most important question may be: when you have a loan from family, when should you pay it off?

It’s a great question, and the answer is often very personal. But there are two major things to consider: The math, and the relationship. If you look strictly at the math, the vast majority of family loans have no interest rate at all. If your loan is like that, it is tempting to shuffle it to the bottom of the list, below credit cards, car loans, and even mortgages and student loans. And if it was purely a mathematical decision, that would make sense. The loan isn’t costing you any more money, so it makes sense to concentrate on all of the other loans you have that arecosting you money.

But it isn’t just a mathematical decision, it is a personal relationship decision, too. While many family lenders are perfectly happy to wait for a long time to see their money back, lent money can create a strain on relationships. As you are considering how to build your debt repayment plan, seriously consider the damage it may be doing to your relationship. If you feel that it is going to cause lasting harm, you might decide to put it higher on the list. But also consider what would make the situation better for both parties. Perhaps paying a minimal amount, but doing so regularly would show how serious you are about paying the money, and may lessen the tension without requiring you to put your credit card repayment plan on hold.

Or you may decide to hold a meeting with your parents, and have an open and frank discussion about your situation. Communicating your situation and plans with them, and then bringing them into the decision-making process may also be a really helpful step. But always consider, if this money is really standing between you and a good relationship with your parents, perhaps it is time to get serious about prioritizing your loan with them.

There is no right or wrong way of paying back family, but taking a look at the practical method, then examining how it will affect everyone involved and making sure there is good communication will make sure you find the best solution for you and your family.

Related

Debt Avalanche Method

The debt avalanche or ‘debt stacking’ method pays off your debts with the highest interest rates first. Unlike the debt snowball, which focuses on balances, the avalanche method focuses on interest rates.

Start a Hustle for Extra Income

Extra income can help you speed up your debt payoff. This article highlights six side hustles to earn extra income without a lot of time.

6 Ways to Up Your Financial Game Now That You’ve Got a Debt Payoff Plan

You've crushed your debt-free planning using Debt Payoff Planner. These six tips from debt payoff champ Kelly Blodgett are great next steps to consider.